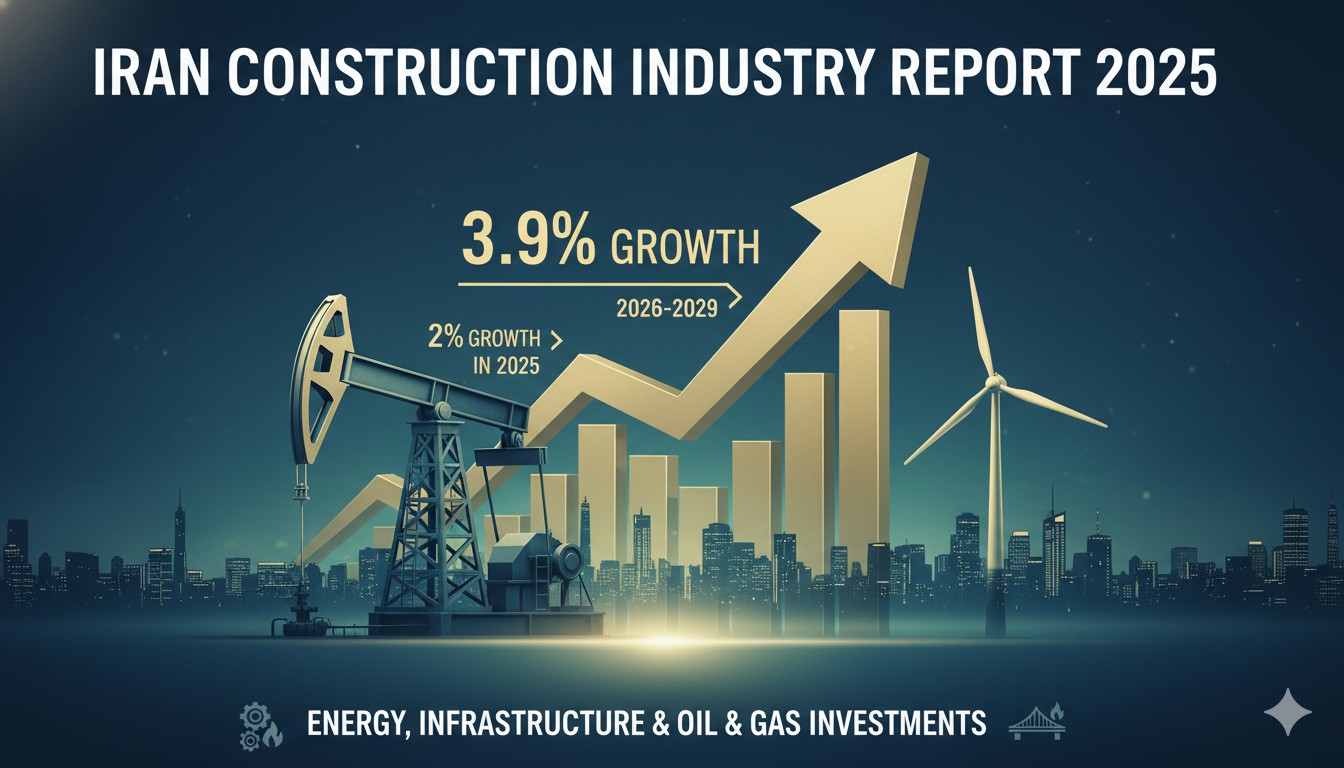

Iran’s construction sector is poised for steady expansion, with real-term growth of 2% anticipated in 2025, followed by an annual average growth rate (AAGR) of 3.9% from 2026 to 2029. This trajectory is primarily fueled by substantial investments in energy projects, infrastructure development, and the oil and gas industry, alongside contributions from industrial, transport, and housing segments. Government initiatives in renewables, nuclear power, and petrochemicals, combined with efforts to attract foreign direct investment, position the sector for sustained momentum despite ongoing economic challenges.

Detailed Sector Outlook and Drivers

The Iranian construction industry has demonstrated resilience amid persistent headwinds such as inflation, currency fluctuations, and geopolitical pressures. Following a period of modest performance in prior years, the sector achieved a projected 2% real-term growth in 2025, marking a stabilization and modest rebound. This performance reflects targeted investments that offset some domestic constraints, particularly in energy-related developments.

Looking ahead, the forecast AAGR of 3.9% over 2026-2029 represents a clear acceleration. Key drivers include heavy capital commitments in the energy sector, where the government is prioritizing diversification and capacity expansion. Plans to boost renewable energy capacity to 10GW by 2030, from around 3.2GW in late 2025, involve significant solar and other clean energy projects. Additionally, agreements for constructing multiple nuclear power plants aim to achieve 20GW of nuclear capacity by 2040, creating extensive opportunities for specialized construction activities.

The oil and gas sector remains a cornerstone of growth. Massive investments—totaling billions in upstream contracts—focus on maintaining and expanding production at major fields like South Pars. Recent deals worth over $12 billion for new developments and optimizations target incremental output gains, necessitating new pipelines, processing facilities, and related infrastructure. Broader commitments, including $130 billion allocated to joint oil and gas fields, underscore efforts to secure resource shares and enhance extraction efficiency. These projects require substantial civil engineering, fabrication, and installation work, directly benefiting the construction industry.

Infrastructure investments further bolster the outlook. Transport projects, including rail expansions to increase the modal share to higher levels, alongside port and road developments, demand ongoing construction input. Housing initiatives continue to address domestic needs, supported by government programs and increased lending for residential builds. Industrial segments, particularly petrochemical expansions, also contribute, with plans to scale production capacities driving factory and plant constructions.

Sectoral Breakdown and Growth Contributions

Energy and Utilities : This segment leads growth, driven by renewable targets and nuclear ambitions. Solar plant constructions and grid enhancements form a major pipeline, while nuclear developments involve complex engineering feats.

Oil and Gas : Upstream and midstream projects dominate, with field developments, pressure maintenance, and export-oriented infrastructure requiring heavy civil works and specialized builds.

Infrastructure (Transport) : Rail, ports, and highways see steady activity, aligning with national connectivity goals.

Industrial : Petrochemical and manufacturing expansions fuel demand for industrial facilities.

Housing and Residential : Supported by policy-driven builds and private investments, this provides baseline stability.

Key Economic and Investment Context

Government strategies emphasize attracting private and foreign capital, including through free zones and incentives for energy projects. Rising foreign direct investment in select areas, alongside domestic financing reforms, helps mitigate sanction-related limitations. While nominal market values show stronger nominal gains due to inflation—such as projections reaching multi-trillion IRR levels—the real-term focus highlights sustainable expansion.

The sector’s performance ties closely to broader economic stabilization efforts, where energy export revenues and production uplifts play a pivotal role. Challenges persist, including material cost pressures and supply chain issues, but targeted investments in high-priority areas provide a buffer.

Overall, the 3.9% AAGR forecast reflects a pragmatic path forward, anchored in strategic energy and infrastructure priorities that promise long-term structural benefits for Iran’s construction landscape.

Disclaimer: This is a news and analysis report based on industry trends and forecasts. It does not constitute financial advice or investment recommendations.